Published 9/17/05.

For all those readers who have slept through the last week, the Optimist is excited to tell you that the price of gold has surged to $460, its highest price in almost two decades. Speaking of sleeping, however, the price of silver has been disappointingly dull compared to gold. Although everyone knows that silver will more than double from its current price of $7.20, and will eventually multiply by a factor with one or more zeros (i.e., 10, or 100, or 1,000, etc.), the key question everyone asks is when the explosion will happen. It seems like most silver investors keep their bags packed for the rocket trip, but they want to wait to purchase the ticket until just before ignition and liftoff. The Optimist admits, of course, that his guesses about a date are no better than those of the readers, but he hopes to provide perspective for recognizing the ignition process so we can all enjoy the liftoff which will soon follow.

When there is a shortage of real physical silver

The Optimist must confess that he thought the rocket was ignited 18 months ago, and he briefly enjoyed illusions about what would be done with all the profits from the silver explosion. That sweet dream was rudely terminated by the subsequent market action, and the Optimist is now as cautious as everyone else about shouting that there are visible flames at the base of the silver rocket. In retrospect, it is now easy to see that throughout the rapid price increase in April 2004 there was adequate physical silver for continued manufacturing and for investment accumulation. That availability of real physical silver enabled the banks and the Comex paper printers to flood the market with paper silver and to drive the price lower. Note that the paper silver didn't actually create any real physical silver. It only saturated the investment demand for people who prefer to bet on the direction of silver prices than to hold physical silver in their possession. The key concept is that the paper silver operation would not have had any chance to drive the price of silver lower if there was not enough real physical silver available for consumption by manufacturers and for accumulation by some investors. The answer to when the price of silver will explode is when there are problems with industry and investors getting all the real physical silver that they need or want. No amount of pretend paper silver will make a real physical shortage go away.

So, when is that, exactly?

The next question readers will impatiently pose is exactly when will there be an unsatisfied physical silver demand. Readers will not be surprised with hearing yet another deficient answer. It isn't just that the Optimist doesn't know the date. If anyone did know the date when demand for real physical silver will overwhelm supply, they would be very unlikely to write about it on the Internet. They would instead be much too busy raising all the cash possible so they could purchase a maximum amount of real physical silver before that explosive date. The Optimist hopes, however, that he can provide a window on one of the key market dynamics that may help us to see when the ignition process is underway. Before opening that window, a little more background will be helpful.

The key is made of base metals

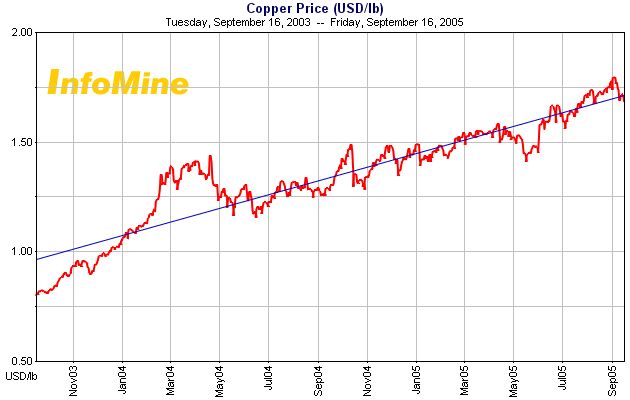

Readers are, no doubt, familiar with the ongoing silver supply-demand deficit, and with the portion of mining production that derives from base metals like copper, lead, and zinc. Approximately 60% of the amount of silver mined is a byproduct from these base metals. During times when more base metals are mined, the amount of byproduct silver which is dumped on the market as additional physical supply is proportionately increased. As one might guess from looking at a chart of energy prices, the world economy has been intensely hungry for energy, and for base metals. The rising prices of base metals over the past three years testify to the increasing worldwide demand for more base metals. It should be no surprise to any reader that rising prices of base metals cause mining companies to ramp up production to keep up with the demand (and to multiply their profits in the process). Consider the three charts (from InfoMine.Com) of lead, zinc and copper below, and you can be sure that base metal production has increased substantially in response to rapidly rising prices.

Silver shortage delayed

The increased production of base metals in response to rising prices resulted in significantly greater production of byproduct silver. Base metal miners don't care about managing the impact on the silver market, so they just dump that excess silver production into the market. The increased amount of byproduct silver meant that there was little risk of running out of real physical silver over the last three years, so the banks and the Comex creators of paper silver shorts could proceed without concern about being tripped up by the physical market. By comparing the three charts above to the comparable chart of silver below, it is easy to see that the rapidly rising base metals prices have had a constrictive impact on the price of silver.

It looks like the sharp increases of zinc and copper prices from May to September have contributed to the recent silver price doldrums even as gold has thrust into new highs for this move.

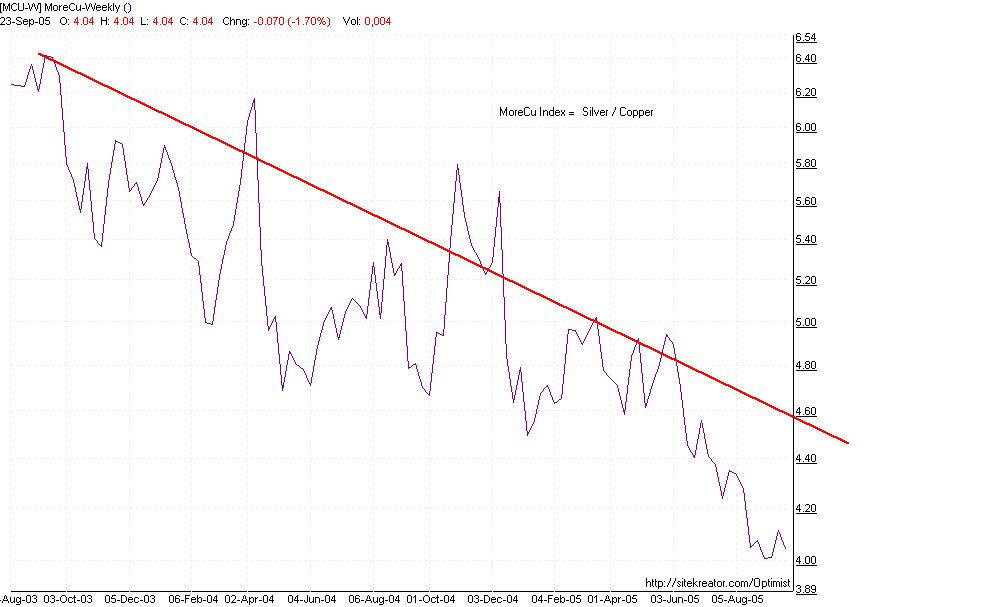

Introducing the MoreCu Index

Another way to view the relationship between silver and base metal prices is through a ratio. Everyone is familiar with the gold to silver ratio, even if silver bulls continue to be depressed by the faster price escalation of gold. Since silver is frequently thought of as more of an industrial metal rather than as a precious metal, another useful ratio is the price of silver divided by the price of copper. The Optimist calls this the MoreCu Index, because it shows more about the impact of copper and base metals on the price of silver. The rational for viewing this index as significant is that when base metal prices are rising rapidly due to industrial demand for base metals, then the additional byproduct silver produced will cause the price of silver to fall in relation to the base metals. If the price rises were due primarily to inflation, then one would expect the inflationary effects to be comparable to both base metals and to silver, so the ratio would be relatively little changed. Let's take a look at the Optimist's chart of the MoreCu Index: